705-998-2017

705-998-2017 vpm@visture.ca

vpm@visture.ca

How to Evict a Tenant in Ontario: A Guide for Property Owners

Eviction in Ontario: What Every Landlord Needs to Know

Owning rental property in Ontario comes with many responsibilities, and one of the most difficult tasks you may face as a landlord is evicting a tenant. Evictions are governed by the Residential Tenancies Act, 2006 (RTA) and overseen by the Landlord and Tenant Board (LTB). The process is not fast, and mistakes can set you back months.

At Visture, we’ve helped countless property owners manage difficult tenancies. This guide outlines how to legally evict a tenant in Ontario, what forms you must use, how long the process takes, and what pitfalls to avoid.

When You Can Legally Evict a Tenant in Ontario

You cannot remove a tenant in Ontario just because you want to. The RTA only allows eviction for specific, legally recognized reasons. The most common include:

- Non-payment of rent

- The tenant owes rent and hasn’t paid within the deadlines.

- Persistent late payment

- Even if arrears are cleared, chronic lateness is grounds.

- Serious damage to the rental unit or building

- Beyond normal wear and tear.

- Illegal activity

- For example, running an unlicensed business or illegal drug activity.

- Interference with reasonable enjoyment

- Repeated disturbances to neighbours or the landlord.

- Landlord’s own use

- You, an immediate family member, or a caregiver need the unit.

- Demolition, conversion, or major repairs

- If the property is being torn down, converted to non-residential use, or substantially renovated.

Important: You cannot evict a tenant because you dislike them, because they filed a complaint, or for discriminatory reasons. Every eviction must follow the letter of the law.

Step 1: Serving the Correct Notice

The eviction process starts with a formal notice to terminate tenancy. Each reason has a specific notice form and rules.

- Form N4: Non-payment of rent.

- Form N5: Disturbances, damage, or overcrowding.

- Form N6: Illegal acts.

- Form N7: Serious problems such as safety risks.

- Form N8: Persistent late payment.

- Form N12: Landlord’s or family’s own use.

- Form N13: Demolition, conversion, or repairs.

You must:

- Use the correct form.

- Fill it out completely and accurately.

- Serve it properly (hand delivery, mail, courier, or posting on the door in specific circumstances).

Example: For non-payment, Form N4 gives the tenant 14 days (for monthly tenancies) to pay or move out. If they pay everything owed within that time, the notice is cancelled.

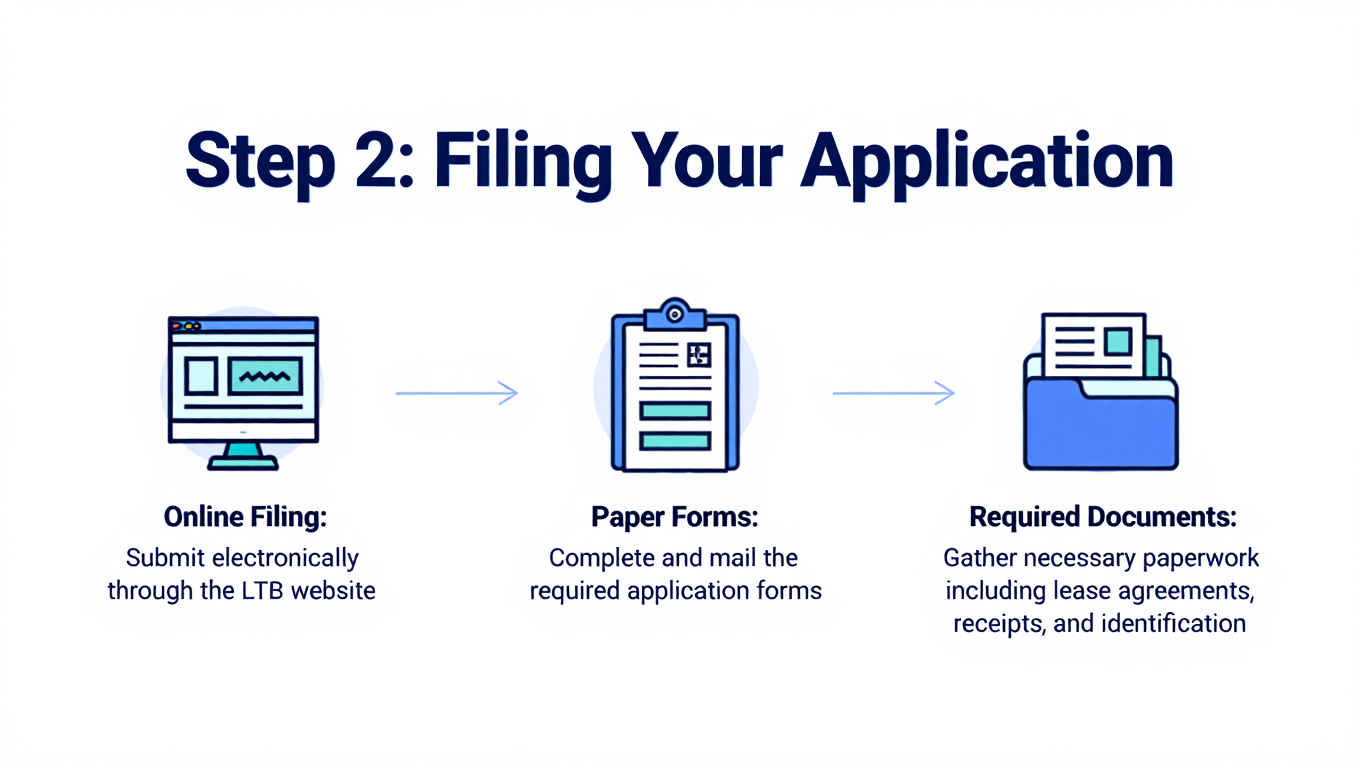

Step 2: Filing an Application with the Landlord and Tenant Board

If the tenant does not move out or fix the problem within the notice period, you then apply to the LTB for a hearing.

- File the appropriate application (e.g., L1 for non-payment, L2 for eviction for other reasons).

- Pay the filing fee (currently about $201 online).

- Submit a copy of the notice served.

The LTB will schedule a hearing, usually several weeks or months later.

Step 3: Preparing for the Hearing To Evict a Tenant in Ontario

This is where many landlords fail. You must bring evidence, not just accusations. The Board will dismiss cases if your paperwork or proof is weak.

Gather:

- Copies of the lease.

- Rent ledger or payment history.

- Photographs or video of damage.

- Written complaints from neighbours.

- Copies of communication (texts, emails, letters).

- Proof that the notice was served correctly.

If you’re claiming eviction for personal use, be prepared to testify and provide affidavits that you or your family genuinely intend to move in for at least one year.

Step 4: The Landlord and Tenant Board Hearing

The LTB hearing is like a small court proceeding.

- You (or your property manager or lawyer) present your case.

- The tenant has the right to defend themselves.

- A Member (decision-maker) listens to both sides.

Possible outcomes:

- Eviction order granted (with or without conditions).

- Order to pay arrears with no eviction if the tenant agrees to catch up.

- Dismissal if the Board finds your application invalid.

Hearings are often delayed due to LTB backlogs. Be prepared for the process to take several months.

Step 5: Enforcing an Eviction

Even if you win, you cannot change the locks yourself. Only the Sheriff’s Office can physically remove a tenant.

- Once the LTB issues an eviction order, you file it with the Sheriff.

- The Sheriff will serve the tenant with a notice to vacate.

- If the tenant still does not leave, the Sheriff attends and removes them.

Changing locks, cutting off utilities, or removing belongings on your own is illegal and can expose you to damages.

How Long Does the Eviction Process Take?

Timelines vary, but as of 2025 most landlords experience:

- 14 days: Tenant’s deadline on an N4 (non-payment).

- 1–3 months: Waiting period for an LTB hearing.

- 2–6 weeks: Sheriff enforcement after the eviction order.

Overall, expect 3–6 months from serving notice to regaining possession. Complex cases or appeals can take longer.

Common Mistakes Landlords Make

- Wrong form used → automatically dismissed.

- Improper service → notice not valid.

- Not keeping records → no evidence to prove your case.

- Self-help evictions → illegal and costly.

- Assuming verbal agreements matter → the Board relies on written evidence.

Special Rules for “Own Use” and Renovations

If you evict a tenant because you or a family member will move in (N12) or for repairs/demolition (N13):

- You must give at least 60 days’ notice.

- You may have to pay one month’s rent compensation.

- If you claim personal use but do not actually move in, the tenant can sue for bad-faith eviction.

Bad-faith evictions are taken seriously and can result in significant financial penalties.

Tenant Rights During the Process

Ontario law gives tenants several protections:

- They can pay arrears before the LTB hearing to stop an eviction.

- They can dispute your claims at the hearing.

- They must be given proper notice periods.

- They cannot be forced out without an LTB order.

As a landlord, respecting these rights protects you from legal problems and keeps your reputation intact.

Why Professional Management Helps

The eviction process in Ontario is time-consuming, procedural, and unforgiving of errors. At Visture, we often step in after a landlord has lost months due to mistakes.

Professional property management helps because:

- We know which forms apply and how to serve them.

- We maintain meticulous rent ledgers and records.

- We represent you at the LTB with evidence prepared.

- We handle communication with tenants in compliance with the RTA.

In many cases, tenants pay or move voluntarily when they see that a management company is involved and procedures are being followed properly.

Key Takeaways

- Evictions in Ontario are controlled by the Residential Tenancies Act.

- You must have legal grounds and use the correct forms.

- Only the LTB can issue an eviction order, and only the Sheriff can enforce it.

- Expect the process to take several months.

- Mistakes in forms, service, or evidence can cost you time and money.

- Consider professional management to reduce risk and stress.

Final Word from Visture

Being a property owner in Ontario means operating under strict rules. Evictions are not simple, but they are manageable with the right approach. If you’re facing a difficult tenancy, don’t risk doing it alone. At Visture, we combine legal knowledge with practical property management to protect your investment and restore peace of mind.